After its Recent IPO, Should Investors Be Buying Toast Inc. (TOST) Stock?

Share

{kind=link}

Toast (TOST) is a cloud-based, end-to-end technology platform purpose-built for the restaurant community. The company provides customers with a single platform that gives them the tools and features they need to run their business across points of sale (POS), restaurant operations, digital ordering and delivery, marketing and loyalty, as well as team management.

Their suite of software and hardware products is integrated with financial technology solutions, which include payment processing and other products. TOST’s software serves as the restaurant operating system, connecting front of house and back of house operations across dine-in, takeout, and delivery channels.

Today, I will examine TOST to identify if it deserves a spot in investors’ portfolios.

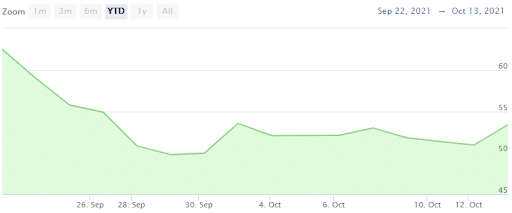

Since its IPO on September 22nd, TOST’s price has declined 13%.

TOST’s top line is growing fast, however, like many IT companies it remains unprofitable

TOAST’s top line has increased consistently over the past year, as the company’s net sales lifted 23.8% in 2020 to $823.1m and are expected to surge by 43.7% to $1.18b this year. However, the company’s costs have grown accordingly on the period, up 13.8% to $682.7m in 2020 and 36.6% to $932.8m in 2021.

This is expected to weigh on the company’s bottom line as analysts are expecting TOST’s net loss to bottom at $358.3m in 2021, compared to a fall of $248m in 2020.

Despite this expected loss, the cash and cash equivalent of TOST reached $518m in 2020 and its recent IPO enabled the company to raise the cash necessary to pursue its growth prospects.

The company is currently trading at a premium compared to its peers, with a P/S ratio of 21.79x. At this price, TOST’s market capitalization looks stretched, given that it is still unprofitable.

The restaurant industry is still a laggard in technology adoption and TOST should benefit from this gap

The end market of TOST has one of the lowest levels of technological innovation across all sectors. According to TOST’s management, restaurants in the United States have spent an estimated $25bn on technology in 2019, which was less than 3% of their total sales, and are expected to increase to $55bn by 2024, which bodes well for the company’s earnings.

Besides, TOST has only 48,000 restaurant partnerships for the moment, representing only 6% of restaurant locations in the U.S. With an addressable market estimated by management at over $15b, TOST has enormous room to grow.

The company continues to invest in its POS platform and has expanded the number of services it offers. With an offering of almost twenty services, ranging from payroll to payment processing and marketing, the company’s retention rates and subscription fees are anticipated to continue to grow at a rapid pace.

In addition, TOST can bank on different sources of revenues, from subscription services, to its financial technology solutions, hardware, and professional services, which will enable the company to increase its profitability.

Take away

I believe TOST is a buy. Growth investors should overlook the company’s inability to turn a profit for the time being, as the company heavily reinvest into the platform and looks to increase their customer base. The $15 billion addressable market points to massive potential for the company in the future. TOST gives their customers innovative solutions that will ultimately lead to the improvement of the business and its bottom line.