An Introduction to Retirement Income Planning

Share

{kind=link}

We all come across many general rules on financial planning in financial media. Understanding such rules provides the intuition behind how we make sound financial decisions—a reason why we will discuss them here in the first place. Nevertheless, while helpful, general rules are insufficient to meet our financial needs. An issue with general rules is that the “one-size-fits-all” approach does not consider differences in our situations. Another is that they tend to make investment recommendations in isolation instead of fully incorporating all aspects of our situations.

When we make financial decisions, we consciously or unconsciously incorporate a variety of factors into our process. Such factors encompass different aspects of our financial and non-financial situations. Instead of accepting general rules published in financial media, we recommend that investors evaluate their own situations before making decisions that fit their needs. For example, one popular rule suggests that investors reduce exposure to stocks after retirement. For a retiree who relies on limited financial assets to support future spending, it makes sense to reduce risk by reducing exposure to stocks. For a retiree—among the lucky ones—who has a guaranteed pension, the incentive to reduce risk is less clear. He may or may not need to reduce exposure to stocks. A retiree who is financially secure and wants to pass his wealth on to his children, has no need to reduce exposure to stocks. The bequest motive essentially extends the investor’s investment horizon to children.

Common factors we ought to consider in making financial planning decisions include:

- Age

- Current income and income trajectory

- Retired?

- Family

- Financial assets and liabilities

- Human capital

- 401(k), pension, and Social Security

- Real estate ownership and mortgage debts

- Saving and spending behavior

- Investment horizon

- Risk preference (e.g., capital preservation versus capital appreciation)

- Bequest motive

Integrated Planning

We recommend that investors use an integrated approach to make financial decisions like the one shown below in Exhibit 1-1. When investors evaluate their financial situation, they should recognize that their financial capital—financial assets that we own minus any liabilities—is only part of assets. For investors who are currently working or may work in the future, human capital—the value of future earnings from employment—is an asset that may be more valuable than financial assets. For most American families, homes are their biggest tangible assets (these may also be their biggest liabilities when real estate markets fall). Therefore, when evaluating our financial situation, we should consider human capital and real estate along with financial capital. Some investors may also have part of their wealth tied up in other non-financial assets such as stakes in family business, art collections, stamp collections, antiques, and royalties from published books. Investors should include these in their financial planning decisions too.

Exhibit 1-1 Integrated financial planning

For purposes of financial planning, we typically start with taking inventory of our financial situation and then incorporate risk appetite as well as forecasts of returns and risk of different investments. An investor’s financial situation often influences risk appetite. Typically, those who can afford to lose part of their wealth have a higher risk appetite, which is a reason why wealthy investors allocate a higher percentage of their money to risky assets. In other words, wealthy investors have the financial ability to take on more risk. Non-financial situations also influence risk appetite. For example, investors in stable countries are willing to take on more financial risk while those in less stable countries have higher preference for safe-haven assets. Individual personality also has a large impact on risk appetite as well. Some investors have a natural tendency to take high risk while others are far more risk averse. Naturally, investors with high risk tolerance tend to invest more in risky assets than similar investors who are risk averse.

The expected return and risk of different investments too has a large impact on financial planning as well. During stock market booms investors have had high expectations on stock returns and shifted more investments into the stock market. Similarly, during housing booms such as in the early 2000s, many believed that housing prices would always go up and took on home equity loans to finance spending. In behavioral finance, such phenomenon is called recency bias. Essentially, investors are inclined to remember the recent years’ return and extrapolate that return bias into the future. To make rational investment decisions, we should avoid recency bias and make more objective forecasts on expected returns.

When we make a financial decision, we should not take just a narrow decision on what to invest in. Instead, we should make decisions on investments, savings & spending, and life insurance jointly. Life insurance (as well as disability insurance) protects us and our families against possible human capital loss caused by death or disability. In other words, it is a hedge against possible losses of one of the most important assets that we hold. Before we decide what to invest, and where and how much to invest, we need to decide how much to invest through savings. To make savings decisions, we evaluate the trade-off between spending now (instant gratification) or spending later (delayed gratification) and our expected financial needs in the future. The size of the savings naturally impacts the size of our investments for investments that reflect cumulative savings and investment returns. The size of our savings also influences risk appetite. Investors with more savings may be more financially secure to take on more financial risk.

Making Assumptions

A key assumption in determining the amount of savings needed is the amount of spending needed after retirement. After retirement, we rely on returns from financial capital and/or selling of financial capital to support our spending. Retirement income replacement ratio, the ratio of income required for after retirement spending to the income before retirement, is often used to estimate the income needs after retirement. A general rule is that a replacement ratio of 70% is needed to maintain one’s lifestyle. Our required income after retirement is lower than the income before requirement for the following reasons:

- After retirement, we no longer have wages. Therefore, we no longer pay Social Security tax, and our income taxes are lower.

- Part of our wage income is used for savings, which no longer applies after retirement.

- We tend to have lower expenditures after retirement. For example, retirees have lower gas expenses, meal expenses, and clothing expenses as they no longer need to travel to work daily, eat out less, and need fewer business attire.

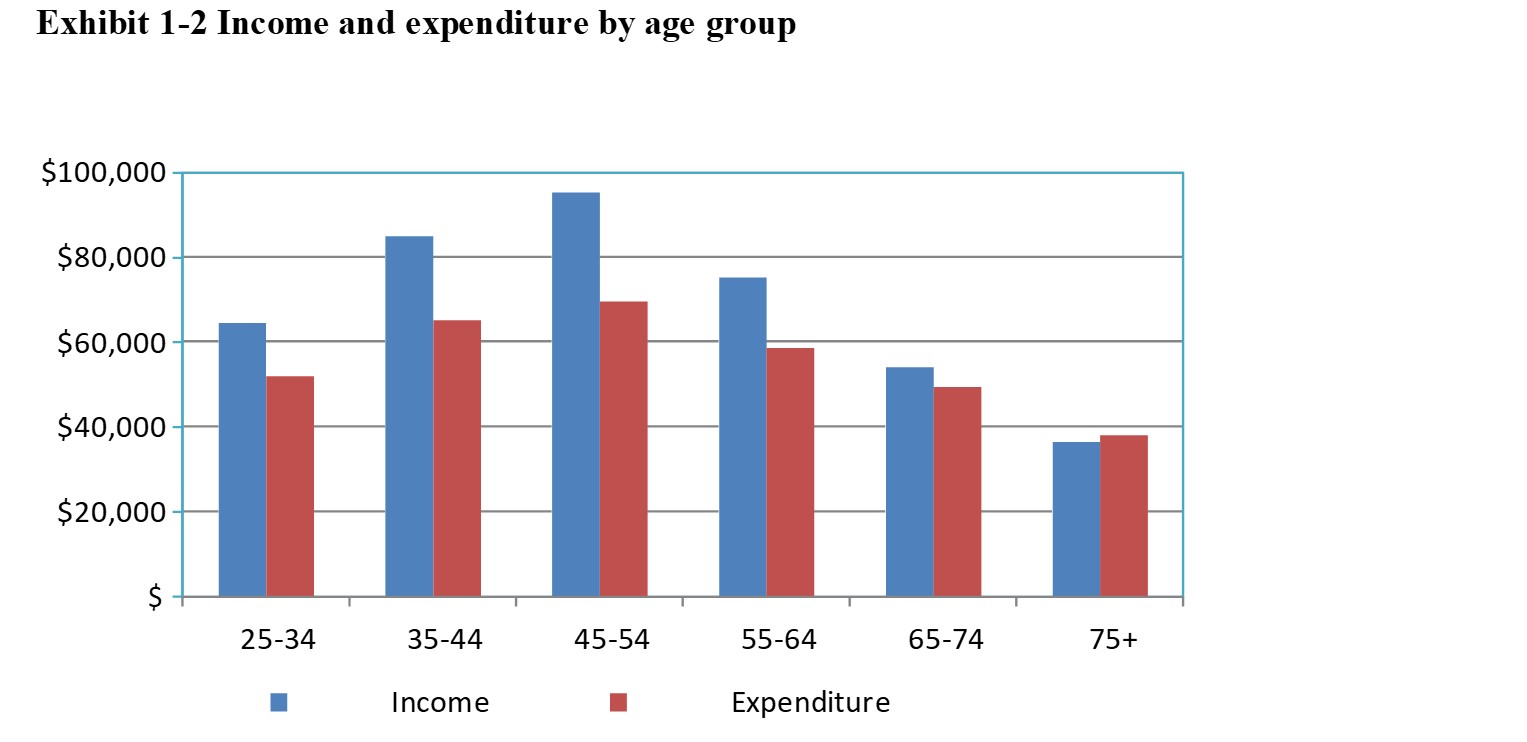

Exhibit 1-2 shows the income and expenditure by age group from a Consumer Expenditure Survey by Bureau of Labor Statistics. The average income of the 65-74 age group ($54,067) was 71.8% of the average income of the 55-64 age group ($75,262) and 56.8% of the average income of the 45-54 age group. Part of the income drop of the 65-74 age group reflects the generation gap: the younger generation—people in the 45-54 age group—had higher productivity and higher wages—than people in the 65-74 age group.

Exhibit 1-2 Income and expenditure by age group

The 70% target is indeed close to the pensions that public-sectors employees receive if they work long enough to get a full pension. The years of full service required for full pension is often 30-35 years.

Retirement Income Support

Such pensions are structured as defined benefit plans. The retirees receive pension benefits determined by a formula based on the years of service and wages received during the service. The benefits do not depend on the performance of the underlying pension funds. Most private-sector employees have no pensions from their employers. Instead, they rely on Social Security, defined contribution plans (401k with possible matchings from employers), and other financial assets for their retirement. For defined contribution plans, employers make annual contributions determined by a formula. The benefits depend on the performance of the underlying funds that employees choose. The key difference between defined benefit plan and defined contribution plan is the entity that bears the investment risk and longevity risk. Longevity risk is the risk that pension recipients live longer than because of increasing life expectancy, which increases the pay out to the recipients. For a defined benefit plan, it is the employer (pension provider) that bears the risk; for a defined contribution plan, it is the employee (pension recipient).

Although private-sector employees typically do not have defined benefit pension plans from their employers, Social Security serves as a defined pension plan for many workers. The replacement rates for average workers from Social Security are 50-60%. The number, however, is substantially lower for employees with high income. Established after the Great Depression, Social Security provides retirees with a safety net after retirement. It is not meant to be a risk-free investment plan for high-income earners. Therefore, it limits the amount of earnings subject to taxation for a given year. When they retire, they do not receive additional benefits on the extra income either. Besides, Social Security is funded on a pay-as-you-go basis. Instead of having a prefunded national pension fund that supports the pay out, the benefits are funded by new contributors’ Social Security tax. As the population ages and life expectancy increases, annual Society Security payments have surpassed annual contributions. It is likely that the Social Security tax will go up in the future or the benefit will have to go down, or both.