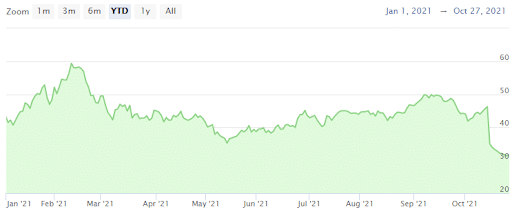

Down 30% in the Past Month, Is Duck Creek Technologies (DCT) a Buy?

Share

{kind=link}

The insurance landscape is rapidly reshaping, as customers’ needs continue to evolve. With innovative products and a greater focus on prevention, new competitors are adding to the competition and increasing pressure on incumbent insurers.

Today, we will explore one of the companies that is raising the standards in the insurance industry and that is well-positioned to become a major player in the sector: Duck Creek Technologies Inc. (DCT).

DCT became an independent company in the summer of 2016 after several years as a subsidiary of Accenture and went public in August 2020. The company is a software as a service (SaaS) provider of core systems for the property and casualty (P&C) insurance industry that offers a single, unified suite of insurance software products, enabling insurance carriers to navigate uncertainty and capture market opportunities faster than their competitors. Duck Creek’s functionally-rich solutions are available on a standalone basis or as a full suite, and all are available via Duck Creek OnDemand.

This year, DCT’s stock plunged 31% over the past month, after a sell-off that was triggered by its latest quarterly report.

With a healthy top-line growth, the software specialist is still struggling to deliver a profit

The company’s finances are in a poor condition. Analysts are expecting net sales to surge in 2021, up 22.2% year-on-year to $259m, and should continue to advance rapidly in the next two years, up 13.5% to $294m in 2022 and up 15.6% to $340m in 2023. Yet, in terms of its bottom line, the software specialist could remain unprofitable for the foreseeable future. Indeed, with a net loss of $173m in 2021, which should accelerate to $259m in 2022, DCT is struggling to deliver a profit.

Despite a cash position of $265m in 2021, down 32.1% year-on-year, DCT has slightly more than one year before it will have to raise more cash by issuing new shares or debt to remain afloat.

At its current price, DCT’s valuation metrics are overvalued for a company that has not delivered a profit in the past three years. With an enormous 2022e EV/EBITDA of 230x and a 2022e P/B ratio of 6x, the shares of the software specialist are likely to go south. Yet, the company is well-positioned to capitalize on a multi-billion-dollar market.

After DCT’s four-quarter earnings report, the market’s excessive reaction has created a nice entry point to join this pure software-as-a-service player

DCT released its quarterly earnings data on October 14th, posting earnings of $0.02 earnings per share and meeting analysts’ consensus estimates. Revenue for the quarter was established at $70.85m, beating the consensus estimate of $69.0m by 21.5% sequentially. Market participants did not buy into these figures, as a downward gap on DCT’s share emerged after the announcement. Moreover, DCT has surpassed analysts’ consensus on a consistent basis, after the release of four consecutive quarterly EPS beats. In the past years, the company has delivered a year-on-year growth north of 20% per year and is closer to reaching a positive bottom line. In this context and despite overvalued valuation metrics, this weakness on DCT shares is providing an interesting opportunity to buy this pure Saas play.

In addition, another update that weighed on DCT’s share in the lower first quarter of 2022 and full-year guidance that established just below the consensus. For the first quarter, DCT’s revenue estimates range between $68m-$70m, whereas the company’s full-year forecasts are shy of analysts’ consensus. Indeed, DCT cautioned that its sales should establish in the $292m-$300m range by year-end, which is short analysts’ forecast of the $303m. Even if investors were disappointed by these announcements and some analysts see these weak forecasts as a major slowdown in DCT equity growth thesis, DCT has a history of surpassing analyst consensus and management’s cautiousness could prove a good sign for DCT’s stock performance going forward.

On the other hand, the consensus of analysts is still bullish for DCT. Eight out of ten analysts following DCT’s equity story have a buy recommendation and the average 12-month target price stands at $50 per share, representing an upside of 59.39% from its current price.

Conclusion

DCT shares have been battered after the company’s fourth-quarter earnings, as the stock dipped more than 30%, following weak revenue guidance.

That being said, I am bullish on DCT in the long term and believe this dip is an opportune time for investors to add this stock to their portfolio.

While the company has not yet delivered a profit, it is slowly approaching its breakeven point, which should provide support to its stock performance. Management’s conservative revenue stance looks like an opportunity for buying this pure SaaS player that is paving the way towards the implementation of new standards in the insurance industry.