My 2 Cents On Powell’s 1% Rate Hike

Share

I try not to editorialize too much in this space, but today I’m going on a small screed. I simply want to ask…

What the hell is the Fed doing?

No need to bury the lede; Chairman Powell should raise rates a full 1% (100 basis points) next Wednesday and then shut up and stand down for the next year.

Actually, my real point is the housing market is due for a major correction and that will have major ramifications for the stock market over the next 6-12 months.

Questioning the Fed is not new or solely being asked in some small corner of finance or a small circle of academia; the central bank’s control of monetary policy has become a pervasive part of how the economy functions. Since the financial crisis back in 2008, the Fed’s actions have become the singular driver for asset prices.

That period covers… four administrations, three Fed chairs, two recessions, and one policy error after another as the Fed has gotten nearly zero right since the turn of the century.

And now, they are about to make another mistake.

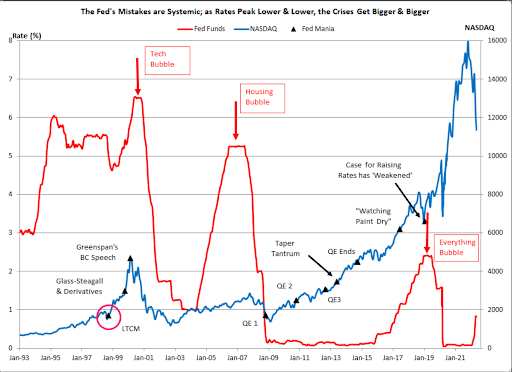

Here’s a quick snapshot of the major market events and the Fed’s reaction over the past 30 years.

Yes, in hindsight it is easy to make the right choice, but when an institution of well paid, highly credentialed people fail to have any foresight over and over again, it’s time to question the value of said institution. The pattern seems to be: act late, break something, throw money at the problem, creating an ever greater challenge of extricating ourselves from the initial problem.

Should we end the Fed? Probably, but at the time I don’t have a better mousetrap for managing the bloated balance sheet and rickety plumbing that our financial systems run on.

The Fed is supposed to have a dual mandate — keep currency/inflation stable and under control and keep unemployment low. They have failed miserably.

The Fed has had a target of 2% inflation since whenever. Yet inflation has been running at over 4% – 9% for more than 18 months. During that period, the Fed purchased $657 billion in mortgage backed securities and $823 billion in Treasuries.

Join the Options360 community today!

The U.S. dollar has risen over 20% in the past year, and they are trying to engineer a situation of massive layoffs to cool wage pressure.

This is a clear example of the cure being worse than the disease. In what world is the pain of inflation worse than losing your job?

All signs point to inflation being transitory. Unemployment becomes embedded.

Gee, I was struggling to make ends meet, and now I’m unemployed and have no money. But thank goodness the wage I might have received has been tamped down!

If the Fed is truly data dependent, why don’t they see that prices on everything from steel, copper, soybeans, wheat, lumber, gas, oil, shipping containers are all down some 40% from their June peak prices?

The lone outlier is housing costs. Shelter — one of the largest inputs to inflation measure — has remained sticky. We might be entering an inflection point, which could spell pain for stocks but relief for Main Street.

Here is the nut graf: The housing market is about to see a major realignment. This will have huge implications for both Wall Street and Main Street.

In the wake of the housing bubble, institutions like BlackRock (BLK) have scooped up real estate, especially single-family homes, removing inventory and exacerbating the sky-high home prices. This supply/demand dynamic is about to flip.

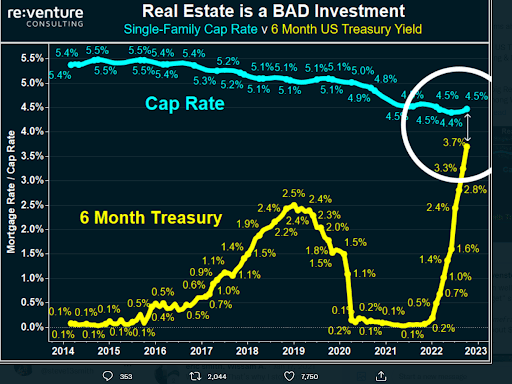

Here is the most important chart you’ll see for the remainder of the year.

The six-month U.S. Treasury now yields basically the same as buying and renting out a house in the United States. The capitalization rate (cap rate) is the expected return on a real estate property. It now sits around 4.4%. Meanwhile a relatively risk free six-month T-bill offers a 3.8% yield.

{kind=link}

If you’re an institutional money manager — such as an endowment or pension fund which have defined hurdle rates of 65% – 67% per year to meet their payout obligations — why would you not shift allocations out of real estate or even equities and into fixed income? The era of TINA (there is no alternative) investing might finally be coming to a close. The great rotation out of equities is about to commence.

Translation: A large selloff is coming. If multiple major institutions start reallocating toward less risky assets (like fixed income) and sell both stocks and their real estate holdings, it will move the market and it will hurt everyday investors.

And while home prices may finally fall, it’s a double-edged sword; housing may become more affordable but only for people that still have a job.

The Fed needs to do one more hike next week, and then exit stage left.