Cracking Modern Portfolio Theory’s Enigma Code with Dedicated Portfolios for Individual Retirees

Share

{kind=link}

During World War II, Nazi Germany developed encryption machines that concealed the transmission of military and diplomatic messages. No one could break the cypher until mathematician Alan Turing and the team at Bletchley Park began cracking the codes. The fact that they had cracked it was kept secret for fear the Nazis would change it.

In investing, modern portfolio theory often appears to investors like an encryption machine. Most portfolio managers use modern portfolio theory to build their models, yet assumptions made by each adviser lead to widely varied models about how successful investing portfolios should be constructed. Over 70 years after Harold Markowitz’s Nobel prize-winning Portfolio Selection, there remains a plethora of interpretations by Wall Street and Main Street firms of modern portfolio theory. These interpretations range from a simplistic 2 Funds for Life approach to David Swenson’s famed Yale Model.

So, which interpretation is the right one for retirees?

Decoding the Origins of the Modern Portfolio

In 1952, Professor Harry Markowitz offered a drastic improvement in portfolio construction by suggesting that the variability of returns should be a factor when comparing one stock with another. It was an explicit recognition of the unpredictability of a stock’s price due to the random nature of market fluctuations in the short run.

Portfolio Selection is considered the origin of “modern portfolio theory” (MPT). Markowitz challenged the standard approach to investing in the 1950’s – that investors should seek the single stock with the highest expected return – was wrong because it did not take into consideration the variance of the returns. Instead, Markowitz posited that investors viewed variance as an “undesirable thing” and any theory attempting to explain how to construct a portfolio should factor both return and variance into its calculations. The improved insight Dr. Markowitz shared changed the investing landscape. Markowitz used the word “investor” without specifying what kind of investor, intuitional or individual, in 1952. This simple insight – which explicitly recognized the unpredictability of returns over the short run due to the random nature of market fluctuations.

In a follow-on piece Individual versus Institutional Investing written in 1991, Markowitz explained that “the ‘investing institution’ which I had most in mind when developing portfolio theory for my dissertation was the open-end investment company or mutual fund.” Markowitz said, “reflection convinced me that there were clear differences in the central features of investment for institutions and investment for individuals, that these differences suggest differences in desirable research methodology, and that a note on these differences may be of value.”

The lion’s share of interpretations of traditional portfolios seems practically disconnected from core individual investor concerns. It is lacking when applied to individuals because individuals have been only tangentially connected to modern portfolio theory. The disconnect is evident in the behavior of investors during significant downturns. This is not due to an investor’s lack of knowledge only. It is also due to the fact that modern portfolio theory was written for institutional investors such as mutual fund companies, pension funds, insurance companies, etc.

So, what about investing for an individual’s portfolio?

Dedicated Portfolios for Individuals

Dedicated portfolio theory cracks the enigma of how to apply modern portfolio theory to personal investors, especially retirees, by focusing on their investing concerns as a major factor in portfolio construction. In the article, “Visualizing U.S. Asset Class Returns Based on Time Horizons, Size, and Style: Safety Zones, Danger Zones and the Critical Path,“ Stephen Huxley, a professor at the University of San Francisco and a managing director at Asset Dedication, and Brent Burns, president of Asset Dedication, offer an alternative approach that extends Markowitz’s insights to personal investing.

The alternative approach utilizes dedicated portfolio theory to build a dedicated portfolio that includes the role of time diversity in transforming the interpretation of volatility. Dedicated portfolio theory recognizes an axiomatic factor which modern portfolio completely ignores, namely the investment time horizon or holding period.

Unlike institutions, individuals have goals and finite lifetimes that are directly linked to time. This linkage leads to differences in investment behavior. The study of behavioral finance has been acknowledged to formalize the distinction. The bottom line is that investment strategies for people that take time into account better align with the needs of personal investors.

Dedicated portfolio theory can crack the investing code for the individual in ways modern portfolio theory cannot. Dedicated portfolios align with individuals because they are liability-driven. Investor’s retirement portfolio withdrawals are used to fill the gaps from pensions or Social Security claiming decisions. Because the income needed from the portfolio is varied based on actual projected spending (year 1: $100,000; year 2: $105,000; Year 3: $55,000; etc.) a dedicated portfolio more clearly aligns with individual investors.

Investment Selection and Risk to Individuals: Volatility or Time Horizon?

As Markowitz pointed out, the future is unknown and uncertain, of course, but using past data to determine how asset classes held up in the contours of market outcomes across nearly 100 years is a reasonable way to evaluate asset class characteristics. Referred to as the “historical audit” approach, it relies on the sequences that actually took place in the markets in the past rather than simulating possible sequences the markets might have taken as the Monte Carlo approach does.

Huxley’s and Burns’ dedicated portfolios demonstrate a compelling alternative to the current conventional approach. The alternative approach offered is through building a dedicated portfolio that focuses on time’s role in transforming the interpretation of volatility. Dedicated portfolio theory recognizes an axiomatic factor that modern portfolio largely eschews, time horizon. Individuals have goals and lives that are time-bound, so an investment plan that takes time into account better aligns with the needs of investors.

By evaluating past market data in search of the best, worst-case asset class results (minimax), dedicated portfolios are designed against the worst of past experience. This is in contrast to modern portfolio theory’s focus on the average results of the past. In examining rolling time periods, paradigms emerge as the data demonstrate asset class performance differences cluster by like-kind time frames.

Individuals with a 10-year horizon or 30-year horizon will have vastly different allocations because of time diversification. The dedicated portfolio allocations explain why one-time horizon owns 34% U.S. large-cap or 21% international developed stock in a clear, accessible way. Clarity creates understanding and understanding leads to an investor’s behavioral control because they know why the portfolio functions as it does over time. Dedicated portfolios use asset classes for the highest and best use according to all available historical data. Dedicated portfolios are prioritized and organized by time horizon that can be aligned with individuals’ lives or specific goals.

Individual bonds or target maturity bond ETFs can be used to create a predictable income stream for a specified number of years; typically, the shorter time frames (7-10 years) where stocks work less predictably. But buying bonds and holding them to maturity for the short run nullifies the randomness of market moves and renders them harmless to the immediate cash flow needs. With the short run taken care of, equity investments can be used for the long term.

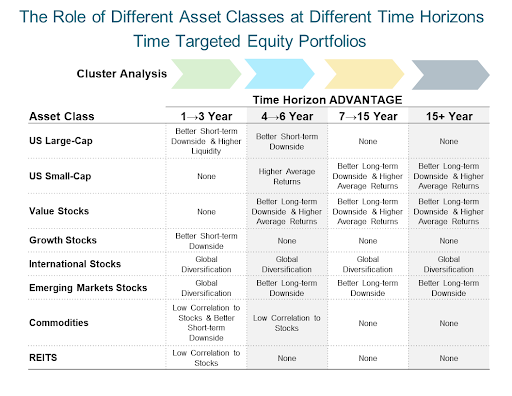

By analyzing rolling time periods, research shows that results tend to cluster into distinct time horizons. The best allocation for shorter bond ladders is different from the one for longer ones. Exhibit 1 illustrates the different characteristics for four different time horizons, ranging from 1-3 years and 4-6 years to the much more common 7-15 year and 15 years or longer time horizons.

Exhibit 1

While past performance is not indicative of future results, past events can point to similar kinds of happenings in the future (depression, asset bubbles, hum-drum cycles, pandemics, war, etc.) and expose the relationship dynamics between events and asset classes. In dedicated portfolio terms, risk is not measured by annual volatility, as it is in traditional modern portfolio terms. Rather, risk is the likelihood that lifetime spending goals will not be achieved. Dedicated portfolio assumptions are weighted to minimize the historic worst-case by the time horizon of the plan. Individuals can take confidence that though their dedicated portfolio cannot predict the future, the portfolio design improves the odds against the deleterious impact that major market declines can have over the relevant time horizon of the plan.

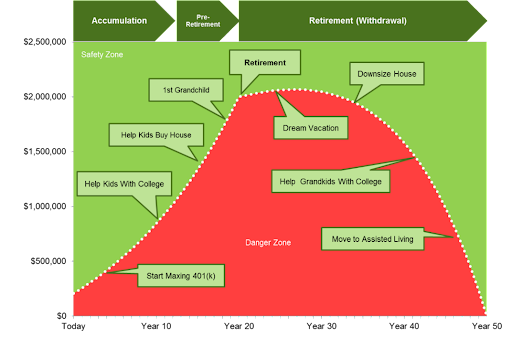

To test an individual’s lifetime spending goals, an analysis called “Critical Path” is calculated as the individual’s benchmark. This is the path or trajectory the plan must follow over time to reach its desired destination (see Exhibit 2). It tests the historical likelihood of success based on customized asset allocation, personal cash flows needed from the portfolio, and the length of time incorporated in the lifetime financial plan, typically 30 or 40 years. The Critical Path calculation simulates the total portfolio asset allocation’s ability to supply the planned withdrawals (inflation-adjusted income and total fees) compared to every historical like-kind time horizon since 1927. While new outcomes are always possible, building the portfolio based on the actual history of the market that includes the Great Depression, World War II, the dot.com Bubble, 9/11, 2008 is used because reliable data is available for that span.

Exhibit 2

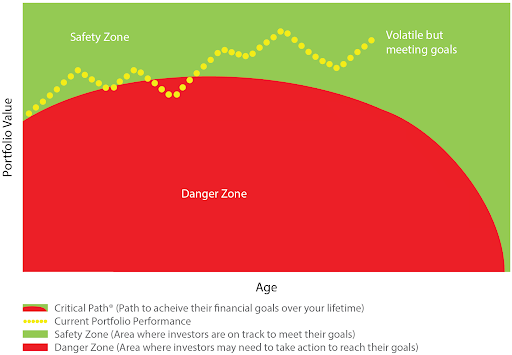

Exhibit 3 illustrates the benchmark functionality of the Critical Path during the Retirement Phase. The portfolio is monitored on a regular basis (see the yellow line), and so long as it stays above the Critical Path, it is in what is considered the “Safety Zone.” That means it will meet all the goals that are defined in the lifetime financial plan. Volatility in the Safety Zone is harmless. This means modern portfolio theory’s focus on volatility is irrelevant and the individual should feel comfortable that everything is going according to plan.

But if volatility drops the portfolio’s value below the Critical Path (that is, drops below its benchmark), it is the signal that action needs to be taken. The allocation of the portfolio needs to be changed, spending needs to be changed, or other goals need to be changed. The Critical Path serves as what statistical quality control engineers refer to as the “control mechanism” that indicates when the process is out of control and needs to be examined to put it back in control, i.e. back above the Critical Path.

Exhibit 3

The Critical Path During the Retirement Phase: the Safety Zone and the Danger Zone

Exhibit 4 summarizes the differences between dedicated portfolio theory and modern portfolio theory, which is the current conventional approach to personal investing.

Exhibit 4

Characteristics of Dedicated Portfolio Theory vs. Modern Portfolio Theory

| DEDICATED PORTFOLIO(ASSET DEDICATION) | CONVENTIONAL MODERN PORTFOLIO | |

| Risk Definition | Lifetime spending needs not met | Volatility, Standard Deviation from the Average |

| Risk Analysis | Probabilistic over like-kind time periods in the history of market since 1927 vs. individual plan, Historical Audit. [Ex. Plan Horizon 30 years, historical audit of every 30-year cycle tested against a retiree’s withdrawal plan.] | Probabilistic, Monte Carlo range of outcomes, Mean-variance optimization (MVO), Standard Deviation |

| Objective Function [Goal to be maximized or minimized] | Bonds: minimize the cost of matching the target spending needs over the chosen horizon Stocks: minimize the possible losses in the Growth Portfolio over a time horizon that works with the Income Portfolio horizon | Risk-adjusted returns. Maximize portfolio expected return for a given amount of portfolio risk, or equivalently minimize risk for a given level of expected return, by carefully choosing the proportions of various assets. |

| Risk Measurements | Percentage of Failure Historically from 1927 & 1947 over rolling client horizon | Standard Deviation, Sharpe Ratio, Treynor Ratio, Sortino Ratio |

| Risk Management Strategy | Time segmentation driven Asset Allocation, Diversification: Bonds for shorter periods and Stocks for long periods | Asset Allocation total return portfolio |

| Portfolio Monitoring for Planning Goals | Critical Path®Client-specific benchmark based on plan goals | Relative to Stock/Bond Benchmark |

Conclusion

Modern portfolio theory is fine for institutional investors. But it was never designed for individual investors who have finite lifetimes where goals change depending on what phase of life an investor is in and how best to handle volatility. Dedicated portfolio theory appears to be a better fit to the fundamentally different investment goals that personal investors face.

Personal investors should thus reconsider blanket acceptance of the role of modern portfolio theory. Instead, they should ask if their portfolios were constructed based on their actual, individual lifetime financial plans or simply part of an enigma code?