Interest Rate Risk in Fixed Income Portfolios

Share

{kind=link}

Similar to an individual, corporations have been capitalizing on the current low interest rates environment to refinance their debt. Where possible, higher interest rate bonds are being called and replaced by securities that potentially yield significantly less. Unfortunately, this has had a detrimental impact on the income generation of portfolios. Investors are facing the unpleasant experience of having bonds called away, and realizing the income-generating potential of their portfolio is significantly less than it has been in the past (this is often known as reinvestment risk). Compounding this problem is the fact that inflation has been running hot, thus remaining uninvested in cash is not an ideal option.

In light of this backdrop, some investors have been forced into dividend-paying equities or have had to make other adjustments to their fixed income portfolios to try to compensate for the lower interest rate environment. Concerning the adjustments made to fixed income portfolios, most of these actions have increased the risk to a portfolio. As such, we believe that it is wise to understand the various risk components of fixed income investments and identify how a portfolio can be constructed to attempt to account for the various risks. To that end, we are focusing on the concept of interest rate risk.

Interest Rate Risk

Interest rate risk relates to the fact that future interest rates might be higher than those prevailing today. This could be considered just an opportunity cost if the investor plans to hold the bond to maturity. However, if there is the potential the bond will be sold prior to maturity, there is the risk of a loss on your investment.

Bonds prices and market interest rates move in opposite directions; they can be thought of as sitting on opposite ends of a seesaw (when one goes up the other goes down). If an investor were to buy a ten-year Treasury bond at 1.30% today at par for $1,000, but in a couple of months the prevailing interest rate environment increased to 1.50%, they would not be able to liquidate the bond for $1,000. Instead, the price would have to fall to a level that makes its yield close to the market rate.

Investors can examine a bond’s interest rate risk through a metric known as duration. Specifically, modified duration represents the percent change in a bond’s price to an instant one percent change in prevailing market rates. For example, a bond with a 4.65-year duration (don’t worry why duration is reported in years), could be expected to see a 4.65% decline in value, if interest rates were to suddenly increase by one percentage point (the opposite also holds). All things equal, bonds with longer maturities have relatively higher durations and are thus more sensitive to changes in market interest rates.

In the current low interest rate environment, some investors are buying bonds with significantly longer maturities in hopes of generating a little more interest income (bonds with longer maturities tend to pay higher rates, all things being equal). This action can significantly increase a portfolio’s duration and interest rate risk; thus, it has the potential to generate losses should the prevailing market rate increase. This is analogous to sitting out further from the fulcrum on the seesaw; the movement that you experience is greater.

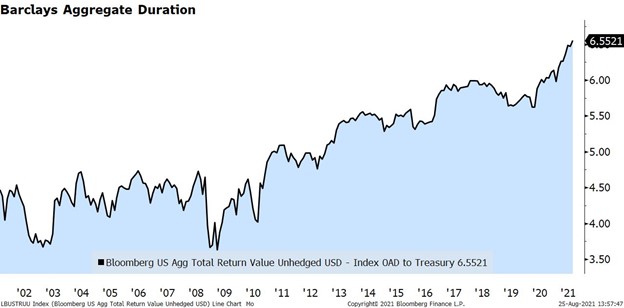

Note that the phenomenon of investing in longer-dated maturities is not just occurring with individual investors but can be found in funds and indexes as well. For example, the Barclays Aggregate Index has seen its duration increase over the last several years, thus making it more sensitive to changes in market rates. As a result, the underlying interest rate risk in many bond mutual funds and ETFs has increased.

It is important to note that a portfolio’s duration is the weighted average of its individual bonds. Therefore, a portfolio’s interest rate risk can be reduced/altered by holding bonds of varying durations. Furthermore, the inclusion of some floating-rate debt, which has extremely low to negative duration, might make sense in certain cases. There are many other portfolio construction strategies (e.g. bullet, barbell and laddered portfolios) that can be deployed in an attempt to maximize returns given anticipated future changes in interest rates, but those are beyond the scope of this article.

In summary, given the current historically low interest rate environment, it is paramount to understand your interest rate risk. Blindly investing in longer-dated maturities to pick up yield might look wise in the short term. However, you must realize you could be scooting out further from the seesaw fulcrum and the drop could be stomach-turning.

Disclosure: This article is provided for informational purposes only. It is educational in nature and not intended to be a recommendation for any specific investment action. None of Private Asset Management, Inc.’s representatives are suggesting that the reader take a specific course of action. Prior to making any investment or financial decision, an investor should seek individualized advice from personal financial, legal, tax, and other professionals. As a reminder, opinions and statements concerning market trends in articles are based on current conditions and are subject to change without notice.