Planning for The American Families Tax Plan, Inflation, the Debt Ceiling

Share

{kind=link}

American Families Tax Plan

On Monday, Sept. 13, 2021, the House Ways & Means Committee released a more moderate American Families Plan tax proposal, restoring some tax rates to the pre-2017 Republican TCAJ Act levels, many of which are set to sunset Jan. 1, 2026, in any event.

The plan was first released in April with higher tax rates and the controversial elimination of the step-up in basis for assets transferred at death. It was a starting point in negotiations, primarily with Democratic moderates since Republicans, at least publicly, claim to be opposed to any changes in the tax laws. The new plan is much closer to a final form than the April release.

Income Tax Changes

A major difference between the new plan and the April plan is that the new plan proposes a 26.5% top corporate tax rate instead of 28% (currently 21%, was 35% pre-2018). The new plan also eliminates the April proposed tax on unrealized capital gains for bequests, preserving the tax-free step-up at death. To make up for those differences in planned revenue needed to cover the infrastructure bill, the new plan lowers the thresholds for some tax brackets and adds some additional taxes to ultra-high earners.

The new plan, as with the April plan, sets the top tax rate back to the 39.6% pre-2018 level starting in 2022, up from the 37% 2018 TCAJ level. The new plan lowers the threshold for the higher rate to $450,000 for married filing jointly from the current $628,300. There is also a proposed additional 3% surtax for high-earners with income over $5 million, raising their top rate to 42.6%. The current 3.8% NIIT surcharge on investment income continues to apply to anyone with investment income stacked on top of ordinary income over $250,000.

The new plan changes the top capital gains tax from 20% to 25%, down from the April proposal of 39.6% — an important adjustment to the plan for all investors. The current top capital gains rate is 20% for gains stacked on ordinary income over $500,000. The new plan lowers the threshold to $400,000. Most of us will continue to pay the current 15% capital gains rate. The 1997 Tax Relief Act changed the then 28% capital gains rate to the current 20%, so this is the first increase in the rate since 1997.

Retirement Plan Changes

The new plan essentially closes the door on “back door” and “mega-back door” Roth IRA conversions. Direct contributions to a Roth IRA are limited to those with income under $198,000. Currently, anyone can contribute $7,000 after-tax dollars to a traditional IRA, and then, if the traditional IRA has no pre-tax dollars, “convert” the funds in their traditional IRA to their Roth IRA, getting around the income limit to contributing to a Roth IRA. If there are pre-tax dollars in the traditional IRA, then the conversion to the Roth is pro-rata with tax due on the pre-tax portion.

If the plan is enacted, the back door Roth IRA ends this year. Roth conversions of pre-tax funds will still be permitted but the conversion of after-tax funds from the traditional to the Roth account would be prohibited.

The plan would also end all Roth conversions for those with joint incomes over $450,000 starting in the year 2032. So high earners have 10 years to get those Roth conversions completed. Why the delay? Congress is obviously of two minds—they need the tax revenue from the conversions to count against the infrastructure plan for the next 10 years but feel that high earners ultimately should not enjoy this ‘benefit.’ Ah, politics!

A new set of required minimum distribution rules is proposed for those with incomes over $400,000 and pre-tax accounts over $10 million. The proposed new RMD is 50% of the amount in all pre-tax accounts over $10m and less than $20m, and 100% of the amount over $20m, payable in any year; these thresholds are met regardless of age.

This will not apply to very many people, but if it does, it is also a gift that keeps on giving. If you have $14 million in your 401(k) and IRA, your RMD this year will be $2 million of taxable ordinary income. Next year it will be $1 million plus growth [($12 million plus growth minus $10 million) /2], and so on. Also, new IRA contributions are not allowed for accounts over $10 million, though 401(k) and SEP contributions are allowed.

Estate and Trust Changes

A loophole will be closed by the plan that permits the grantor of an intentionally defective grantor trust to benefit from trust assets and pay lower than trust personal income taxes on trust gains while the trust holds those assets away from the grantor’s estate and potential individual estate taxes. This change will also affect the structure of irrevocable life insurance trusts.

More relevant is the reduction of the lifetime exemption for estate and gift taxes. Currently, the federal estate tax exemption is $11.7 million, and with portability, $23.4 million for a married couple. The 2017 TCAJ Act doubled the $5 million exemption to $10 million, with inflation adjustments, and also specified the increase would sunset back to $5 million on Jan. 1, 2026. The new plan will accelerate that reduction to $5 million for individuals, and $10m for married couples by four years to Jan. 1, 2022. The April plan was unsettled whether the exemption would be $5 million/$10 million or $3.5 million/$7 million. $10 million provides more wiggle room. Note that individual states may have lower estate tax exemptions that require estate planning not needed for federal estate taxes.

What’s Next

The new plan seems tailored to satisfy moderate Democrats who are a necessary part of the reconciliation strategy to pass the new Act with a simple majority in the Senate. Depending on how solidly that moderate support stands will determine how quickly and in what final form this bill is enacted.

Meanwhile, a showdown on the Treasury debt ceiling is rapidly approaching a new fiscal cliff.

McConnell has said that Republicans will not support an increase of the debt ceiling. According to Secretary Yellen’s Sept. 8 letter to Congress, the Treasury will exhaust its extraordinary measures to stretch out cash on hand during the month of October, and the United States of America will then be unable to meet its obligations. A shutdown of the government might be the least of it. A default by the Treasury would have a significant impact on domestic and international markets.

At this point, and it should not be surprising given all that has transpired this year, it appears that some in Congress are willing to take significant existential risk to advance their political agenda. The markets will increasingly reflect this uncertainty and insecurity as a default nears.

Markets and Inflation

From the third week of August, the U.S. stock market steadily gained 3.7% and set a new high just before the Labor Day break. In the two weeks since, the market has moved down, giving back about half the gain. Though inflation slowed somewhat in August, which suggests that the Fed will continue its bond-buying stimulus and keep its overnight rate at 0%–.25%. It also means that growth may not be as strong as expected. So in this gap before quarterly earnings reports begin again, the market meanders looking for some sign of future value.

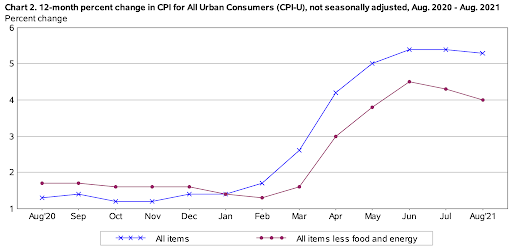

August CPI-U all-items inflation came in at 5.3% for the past 12 months, down slightly from July’s 5.4%. More telling, the monthly change was just 0.3%, following 0.5% for July and 0.9% for June. Inflation is cooling off. Though still high at 5.4% over the past 12 months, the forward rate is now 3.6%.

It appears at the moment that Powell may be right that the inflation spike may be short-term. It’s still early in the recovery, and the Delta Variant is still filling hospitals. There are bumps ahead, so markets and inflation will be choppy. For example, the producer price index is still rising at 8.3% for August, the highest since the index was created in 2010. On the other hand, the historic long-term average for (consumer) inflation is 3.3%. From its June peak, we are turning back towards that level and away from the danger of hyperinflation.