Private Equity in Retirement Plans: Why Now?

Share

{kind=link}

In a surprisingly bold move in June of 2020, the U.S. Department of Labor (DOL) and the Securities and Exchange Commission have indicated a willingness to allow private equity in retirement plans. Private equity has long been a significant component of institutional allocations, including defined benefit plans, but not available in defined contribution or 401(k) plans. This development is motivated by a recognition that private equity offers the potential for higher returns, and consequently would help retirees grow their retirement assets.

This announcement has triggered a number of different reactions – both positive and negative – which we will examine in this article.

What are the merits of private equity?

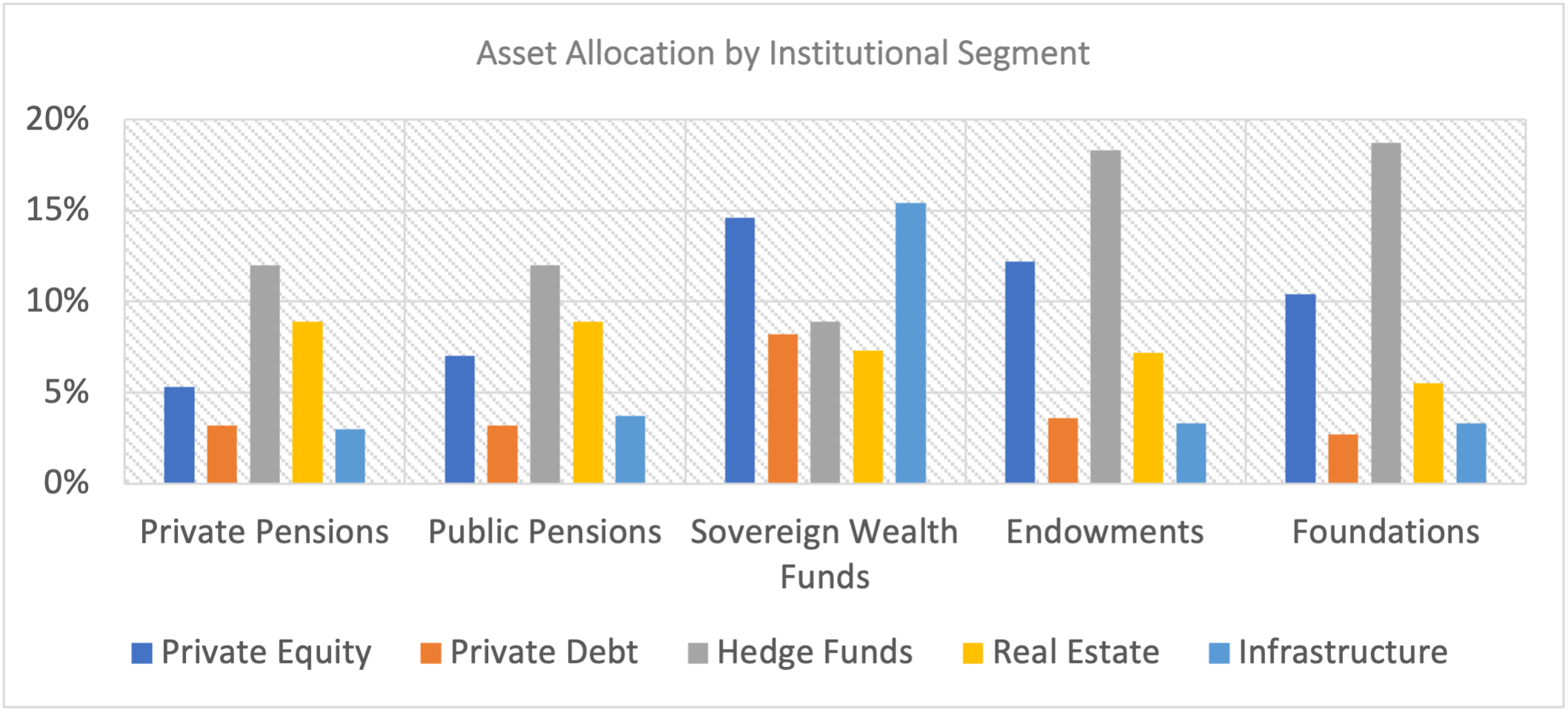

Private equity has long been a significant allocation with large endowments, foundations, pension plans, and sovereign wealth funds (see figure below). The appeal has long been the opportunity for outsized returns, identifying the next Apple, Google, or Facebook, and reaping the rewards when those companies go public via an IPO.

Figure 1, Alternative Allocation by Institutional Segment

Source: Prequin, CAIA Association, 2021

Source: Prequin, CAIA Association, 2021

Private equity has historically delivered a 3-4% illiquidity premium relative to traditional investments. The illiquidity premium is the excess return provided by private equity for locking up capital for an extended period of time. Based on forward-looking capital market assumptions, private equity is projected to deliver returns of approximately 9–10 percent over the next 10 years, a roughly 3 percent illiquidity premium over traditional equity returns. This is due to multiple factors, including the growing number of private companies and the falling numbers of public companies.

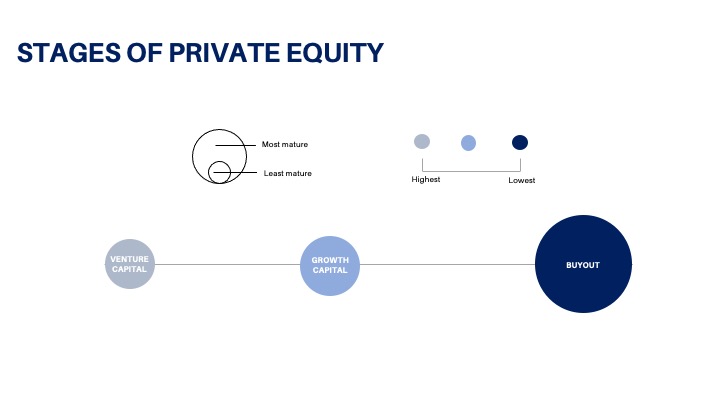

Private equity is delineated by the stage of development, from venture capital to buyout. Each stage represents a different risk and return profile; and consequently, investors should seek to understand the stage of the underlying companies.

FIGURE 2

Venture companies are at an early stage of an idea for a unique product, service, or technology. Early-stage ventures may have little to no revenue and need capital to bring its ideas to life. Founders often seek capital to fund their business plans. Google, Facebook, and Uber began as fledgling companies with ideas that would change the market. They needed capital early on to fund those ideas. When they ultimately went public, they made substantial money for their founders and early investors.

Growth companies have a proven business model, are growing rapidly, and are either profitable or have a clear path to profitability, with revenues growing 20 percent or more annually. Private equity firms typically take a minority stake in the company and work with the management team to help create value through operational improvements and revenue growth, either organic or through acquisition.

Buyout companies have stable revenues and cash flow. A private equity fund purchases firms at this stage through a leveraged buyout and executes a long-term value creation plan, which may involve organic growth, inorganic growth, and operational improvements, before selling the company. These represent the largest segment of private capital.

Driver’s of Returns

Today, there are approximately 3,700 public companies, nearly half the number that existed 20 years ago. Many companies are staying private longer and some choose not to go public at all. The private market universe, by comparison, is quite large and growing, encompassing roughly 98 percent of the largest 185,000 companies. Public companies are also getting older, with an average age of more than 20 years, versus an average of 12 years in 2017. Age matters because company growth typically slows as they mature.

Private companies also have the luxury of planning for the long run. Public companies, by contrast, often suffer from a short-term perspective, struggling to meet quarterly market expectations. Private companies can focus on executing long-term strategies without having to appease shareholders. The results show that this freedom is a substantial benefit. Private equity managers focus on creating value over three to six years. They often bring operating expertise and can help founders develop and implement multi-year plans.

Private companies also benefit from an information advantage. Public companies are required to disclose financial information and key business drivers to shareholders. Most public companies are also widely scrutinized by Wall Street research, so all information is priced into the stock price. Conversely, the private markets are inefficient, and skilled private equity managers can exploit their information advantage to identify attractive acquisitions and execute their long-term strategy without distractions.

What are some of the considerations for retirees?

While private equity offers the potential for higher returns, investors need to consider a number of important factors before investing, including minimums, fees and liquidity among others. The primary investors in private equity were initially institutions and family offices, who were able to lock up capital for long periods of time (7-10 years). They invested in the classic limited partnership structure which was only available to “qualified purchasers”, at high minimums and limited liquidity.

Recently, as I noted in an article title that was published in the November-December, 2019 issue of the Investments & Wealth Monitor titled “Private Markets: Innovation and Evolution,” there have been a number of structural innovations that make private equity more accessible to a larger group of investors. Product innovation has sought to address some of the limitations of the classic private equity structures: accreditation, minimums, and liquidity. Feeder funds, interval funds, and tender offer funds have helped democratize private market investing and address some of the structural limitations.

Classic LP funds are available only to qualified purchasers, typically at higher minimums and limited liquidity. Investors commit capital that is drawn down over time (capital calls).

Feeder funds have become popular with HNW investors because they let investors pool capital and access top-tier funds at lower minimums. Feeder funds are available to qualified participants, who are then subject to capital calls.

Interval funds are available to accredited investors, or even to those with lower accreditation, at lower minimums and quarterly liquidity. They are not subject to capital calls. To meet liquidity demands, interval funds may experience cash drag (the cost of meeting redemption requirements).

Tender funds are available to accredited investors at lower minimums, with liquidity via a tender offer. The board decides how much liquidity they’ll provide and when. They are not subject to capital calls. Tender offer funds are not required to hold liquid assets.

Private equity provides the opportunity for strong returns and diversification relative to traditional investments, but investors should also evaluate the risks before investing. Risks include a lack of transparency compared to the public markets, with investments typically valued on a quarterly basis. Private equity investments are illiquid, and investors should be prepared to stay invested in a fund for the duration (7 to 10 years), even if the fund offers greater liquidity.

In the DOL’s statement, they provided guidance regarding private equity in retirement plans.

- The impact of the private equity allocation on diversification, expected return, and fees on a long-term basis

- The ability of plan fiduciaries to oversee private equity investments, versus hiring an expert consultant

- The percent invested in private equity, noting that the SEC limits illiquid assets to 15 percent for registered open-end investment companies

- Whether plan participants will be permitted to take benefit distributions and move into other investment options

- Agreement by plan fiduciaries to value private equity investments according to accounting standards and subject those investments to an annual audit

- Whether the long-term nature and liquidity restrictions of any private equity investments align with plan participants’ ability to take distributions or change investment options

- The adequacy of participant disclosures regarding the character and risks of a plan investment option that allows investors to make an informed investment decision

There is still work to be done before private equity becomes a viable option for many retirees, but the DOL has acknowledged that these once elusive investments represent valuable tools for retirees. There is a need for better education, more products geared toward retirees, and enhanced transparency.

Allocating to private equity

While private equity represents an attractive opportunity for retirees, investors should carefully consider the risks and structural trade-offs before investing.

- What is the appropriate amount to allocate to private equity?

- How should the allocation be funded (from equity allocation)?

- What is a realistic time horizon for the investment (7-10 years)?

- What is the experience of the fund manager?

- What are the underlying investments (stages of private equity)?

- Does the fund have a ‘cash drag’ to meet redemptions?

Investors may need to consult with their financial adviser and/or retirement plan sponsor to answer these questions. For additional information, please visit https://www.tdavidowconsulting.com/blog.