The Fed is Preventing Negative Interest Rates, and Keeping Money Market Funds Viable

Share

{kind=link}

Here’s a thought experiment. Imagine that you live in the city of Hanover, Germany. Seated in a local café, you are sharing a cup of coffee with your next-door neighbor, Hans. One of the things you know about Hans is that he considers himself to be a pretty savvy investor. As you sip your coffee, Hans begins to describe one of his recent investments. He tells you that he has invested in German government bonds that will mature in 30 years. “These bonds are absolutely safe,” says Hans. “They carry a triple-A rating!”

Instinctively, you conclude that Hans has made a smart investment decision. But then you ask Hans, “What interest rate are you earning on this investment?” Hans replies, “Well, if I hold these bonds until they mature in 30 years, I’ll get back about 5% less than I paid for them.” Hans’ last comment takes a minute to sink in. You ask yourself, did he just say what I think he said? Wait 30 years to lose money?

In August 2019, to help finance its budget, Germany decided to raise money from the sale of government-issued bonds. The government sold €824 million ($938 million) worth of 30-year, triple-A bonds. What was notable about this bond sale is that these government bonds paid investors a negative interest rate of -0.11%. In other words, after holding the bonds for 30 years, purchasers were guaranteed a loss on their investment. In fact, the bond investors will get back €795 million. That makes for a guaranteed loss of €29 million.

You may be wondering, were seasoned investors really interested in buying long-term German bonds that guaranteed an investment loss? Turns out, they were. I remember reading about this bond sale and wondering why there was such a keen interest among investors. I reckoned that there could be only two assumptions investors were making:

- Assumption one: Investors were worried about the possibility of an economic collapse, and, in that event, they could be confident that at least the lion’s share of their money would be safe, or,

- Assumption two: Investors assumed that future long-term interest rates would fall even further into negative territory making it possible to “flip” the bonds for a profit.

It’s been only 2 ½ years since the German bonds were purchased, so we’ll have to wait and see if either assumption proves correct. However, negative interest rates have remained a fact of life in Germany as well as the other 18 Euro-area nations. The short-term interest rate in Germany is now -0.57%. Savers in both Japan and Israel also face having their cash invested at interest rates below 0%.

Some in the U.S. were fans of negative interest rates. After watching Germany sell its bonds for below 0%, then President Donald Trump tweeted:

“Germany sells 30 year bonds offering negative yields. Germany competes with the USA. Our Federal Reserve does not allow us to do what we must do. They put us at a disadvantage against our competition. Strong Dollar, No Inflation! They move like quicksand. Fight or go home!”

How The Fed has Prevented Negative Interest Rates in the U.S.

About the prospect of negative interest rates coming to the U.S., many financial experts were deeply skeptical. Following the German bond sale, Charles Tan, senior vice president and

co-chief investment officer at American Century Investments stated, “We believe negative yields pose an existential threat to our long-standing financial and economic systems by ultimately transferring wealth from savers to debtors. They punish savers, who lose money on their deposits, and they reward debtors, who essentially get ‘paid’ for borrowing money. This undermines the entire premise of our banking systems and financial markets.”

Put me in the camp of people who believe negative interest rates would be bad for the U.S. The Federal Reserve apparently agrees. It has taken bold steps to prevent rates from falling below 0%. In the process, the Fed has perhaps saved the money market industry – and maybe the entire economy – from catastrophe.

Understanding the Reverse Repurchase Agreement

To understand how the Fed has prevented negative interest rates, let me explain a financial transaction known as a reverse repurchase agreement (“reverse repo”). A reverse repo is a contract between the Fed and a “counterparty.” The counterparty could be a bank, an investment management firm, or a broker dealer. Under the terms of the reverse repo, the Fed borrows from the counterparty and, in return, provides collateral to the counterparty. The reverse repo can be for as short a time as overnight, or it can be extended for longer periods.

Importantly, a reverse repo removes liquidity from the financial system. This is crucial because, in recent years, the Fed has injected trillions of dollars of excess liquidity into the economy. When too much liquidity is introduced, one of the possible outcomes is that interest rates can turn negative. That would be bad for the economy and for the money market industry, in particular.

The Role of Money Market Funds

Money market funds are mutual funds that play a crucial role in the financial system.

It’s not difficult to imagine the money market industry facing a potential catastrophe if short-term interest rates were to move below 0%. Moreover, a negative interest rate scenario could well induce a spreading of risks to other sectors of the financial system. To understand why this is possible, let’s review exactly what a money market fund is and the role that it plays in the financial system.

Money market funds are mutual funds that take in money from investors and in turn invest in cash, cash equivalents, and short-term, high-quality debt instruments such as short-term U.S. government debt, CDs, banker’s acceptances, commercial paper, and repurchase agreements for short-term government securities. By virtue of the way they invest assets, money market funds play a crucial role in providing short-term financing for corporations and financial institutions.

Money market funds also purchase substantial amounts of short-term debt of the U.S. government as well as government-sponsored entities like Fannie Mae and Freddie Mac. We’re talking huge dollar amounts here, $4.67 trillion as of December 21, 2021.

Consider what would happen if interest rates plunged into negative territory. Assets would very likely drain away from the money market funds. The profitability of the money market funds would be severely tested. Demand for U.S. government and government-sponsored enterprises debt would plummet. And a crucial source of institutional financing would be jeopardized. A very real risk of financial contagion would present policymakers with a significant new management challenge. Better to avoid this. And this is where the reverse repo enters the story.

The Fed pays 0.05% (5 basis points) interest on its reverse repurchase agreements. This is a tiny rate of interest, to be sure, but it packs a big punch. That is because 0.05% is more than 0%! And it’s more than any negative interest rate. The reverse repo is important, therefore, because it guarantees that the money market funds have a place to invest their assets that pays a positive rate of return. It doesn’t matter that it’s a small return. What matters is that it isn’t a negative return.

The “Reverse Repo” Gets Bigger and Bigger

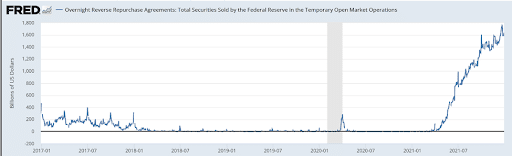

I want you to understand how big and important the use of reverse repos have become. In March 2021, the Fed increased the counterparty limit for reverse repos from $30 billion to $80 billion. In April 2021, the Fed broadened the scope of institutions that can engage with it for reverse repos. Now, in addition to banks and government-sponsored enterprises like Freddie and Fannie, investment managers like BlackRock Advisors, LLC, Vanguard Group, Charles Schwab, and Dimensional Fund Advisors can also participate. These changes should tell you how important a tool reverse repos now represent to the Fed. Their usage has grown exponentially. For context, on January 15, 2021, the Fed had no money in reverse repos. Today it has more than $1.6 trillion!

Reverse repos have skyrocketed to $1.673 trillion as of December 29, 2021. Source: St. Louis Fed

Stock Prices and Reverse Repurchase Agreements

In December I wrote an article entitled “How the U.S. Abandoned Capitalism, And What Took Its Place.” The article explains how The Fed’s use of quantitative easing and the creation of massive amounts of new credit has driven stocks and other asset prices higher and higher. It’s possible, if not probable, that by providing a mechanism to remove liquidity from the financial system through the increasing use of reverse repos, the Fed has prevented asset prices from moving even higher than today’s bubbly stratospheric heights.

I think the Fed is dealing with a tough balancing act. As you know, inflation has reemerged and appears likely to last longer than the Fed originally forecasted. The Fed has also signaled its intent to wrap-up its quantitative easing program by March. After 12 years of asset price inflation, I wonder if the Fed may be setting the stage for an even greater use of reverse repos? We’ll have to wait and see. But by already expanding its use of reverse repos to a level approaching $2 trillion, the Fed has shown us that its creativity can appear limitless. A key question is, will the future reveal that the Fed’s wisdom has matched its creativity?

Author’s note: My thanks to macro economist Richard Duncan for allowing me to use a chart from his video newsletter Macro Watch. Duncan is graciously offering a 50% discount to any reader who wishes to become a Macro Watch subscriber. I highly recommend this newsletter as it is full of original information and valuable insights. If interested in a subscription, enter discount code: Life at https://richardduncaneconomics.com/product/macro-watch/