2 Biotechnology Stocks Wall Street Predicts Will Climb by 90% or More

Share

{kind=link}

After an impressive performance last year, biotech stocks are having a less than stellar 2021. The iShares Biotechnology ETF (IBB) currently only up 4.5% year to date (YTD), compared to the 21% gain for the S&P 500.

Investing in biotech stocks is risky, as a company’s drug candidate can prove to be ineffective or worse. However, when companies are able to create effective drugs, biotech stocks can be big winners.

Today I’m going to take a look at two biotech stocks, Allogene Therapeutics, Inc. (ALLO) and Berkeley Lights, Inc. (BLI), that have been struggling but that Wall Street Analysts believe will double.

Allogene Therapeutics, Inc. (ALLO)

ALLO is a clinical-stage immuno-oncology company, focused on the development and commercialization of genetically engineered allogeneic T-cell therapies for the treatment of cancer. The Company is engaged in developing a pipeline of multiple allogeneic chimeric antigen receptor (CAR) T-cell product candidates utilizing protein engineering, gene editing, gene insertion, and advanced T cell manufacturing technologies.

ALLO’s shares plunged 37% year-to-date and more than 42% in the past month:

ALLO’s bottom line is anticipated to remain unprofitable for the medium term, with a net loss that is expected to slightly accelerate by 2.8% year-on-year to $258m in 2021. Going forward, the company’s loss is expected to continue to worsen, reaching a -$352m in 2022 and bottoming at -$397m in 2023.

After such a massive decline in 2021, investors might expect ALLO’s valuation metrics to be attractive. Yet, the company is trading more than twice its book value, with a P/B ratio of 2.24x and uncertainty is still prevailing as to when the company’s product candidates will hit the market.

This month, the FDA paused ALLO’s clinical trials after a bone marrow biopsy revealed a chromosomal abnormality in one of the patients in the clinical trial for ALLO-501A’s therapy.

However, Wall Street analysts are bullish on ALLO. Twelve out of fourteen analyst recommendations are bullish, with an average target price of $32.50 per share, and the average price target is 103% higher than where the stock is currently trading.

Berkeley Lights, Inc. (BLI)

BLI is a leader in digital cell biology, focused on enabling and accelerating the rapid development and commercialization of biotherapeutics and other cell-based products. The company’s Berkeley Lights Platform captures deep phenotypic, functional, and genotypic information for tens of thousands of single cells in parallel and can also deliver the live biology customers desire in the form of the best cells. Berkeley Lights platform is a fully integrated, end-to-end solution, consisting of consumables, including its OptoSelect chips and reagent kits, advanced automation systems, and advanced application and workflow software.

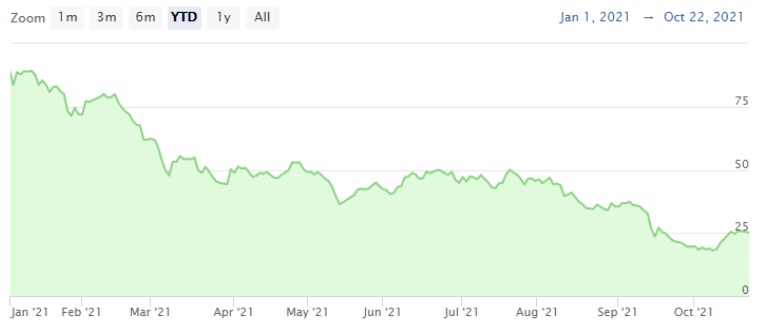

Since the beginning of the year, BLI’s shares have lost a jaw-dropping 72%:

BLI has responded to these allegations in a note to clients where it said that its customers expressed no concern in reaction to the Scorpion’s short report and that the underlying value proposition of BLI’s Beach platform stays intact.

Looking at the company’s financials, BLI is expected to significantly expand its top line this year, up 42.8% year-on-year to $918m. Yet, in 2022 and 2023 analysts’ expectations are expected to drop considerably, with respective net sales figures of $130m and $173m.

The bottom line of the biotherapeutics company is even less persuasive, with a net loss of $624m in 2021 which is estimated to slightly decline in 2022 to $556m. After the massive plunge in BLI’s stock price, the company still trades at a high 2022e P/B ratio of 9.7x and 2022e EV/Revenue of 12.1x.

Despite Scorpion’s report and these poor financials, analyst consensus remains bullish, with 5 buy recommendations out of 6 analysts covering BLI. The average 12-month target price stands at $68.25 per share, corresponding to 167% upside potential from its current price.