2 Bond Funds For Playing A Reversion To The Inversion

Share

My eyes are jumping all over the screen as I scan for opportunities in the market.

Given we appear in the midst of a slow motion train wreck that is the global banking crisis, it probably makes sense to pull back for a big picture look at the macro-economy and funds that represent major asset groups. To say it’s chaotic and confusing would be an understatement.

Bonds have rallied sharply (price up, yield down) and commodities are tanking; both suggesting recession is looming.

On the other hand, equities and major currencies have held steady indicating little to no concern for a broad economic slowdown or turbulence. Large-cap tech has held up especially well; Invesco QQQ Trust (QQQ) is actually up 4.3% since Silicon Valley Bank went into receivership on March 9.

The biggest moves have come in the bond market as forecasts for the path of interest rates have been abruptly recalibrated. We will get some clarity on Wednesday when Powell and the Federal Open Market Committee (FOMC) make a decision on whether or not to continue raising rates.

Just 10 days ago a 50 basis point hike was all priced in. Now, there is a 50% chance it will be just 25 bps and a 15% chance there will be no rate hike at all. Investors had been hoping and begging for a Fed pivot, I don’t think many people thought it would be major bank failures that would cause the pause. No one expected a bank to fail for owning too many ‘risk free’ long-term bonds such as treasuries and mortgage-backed securities.

The change in expectations can clearly be seen in the yield curve; that is the relative interest rates across maturities. Three weeks the spread between the 2-Year Treasury Note, which was yielding 4.67% and the 10-Year Treasury, which was 3.55%, was 1.02 basis points. That was the largest inversion on record. On Monday morning, the 2/10 spread was down to just 15 basis points.

The inverted yield curve, which is typically a signal of an upcoming recession, has been one of most highly tracked and hotly debated aspects since the Fed started hiking rates a year ago. If you recall, the curve first inverted last April. The recent price movements also reflect the largest and quickest reversion or flattening of the curve in history.

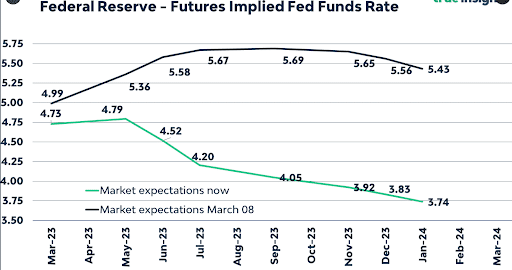

The sudden change in expectations can be seen in the Fed Futures, which had priced in a terminal or final peak in rates at 5.67% in August of this year to having already peaked at 4.99% earlier this month.

The expectations seem to be if the Fed does hike again on Wednesday, that it should be the last rate hike for this cycle. The theory being that fall-out from the banks will take the form of stricter lending standards, more regulation, and the need to offer higher returns on short-term deposits to stem withdrawals.

This will have the effect of tight financial conditions, which should help subdue inflation, the Fed’s primary goal.

This, in turn, should cause a further flattening of the yield curve, back to a normalization in which longer-term bonds pay a higher interest rate than shorter-term.

Two popular bond ETFs I’m keeping an eye out for are the iShares 1-3 Year Treasury (SHY), which is a proxy for the 2-year and the iShares 20+ Treasury (TLT), which is a proxy for the 30-year bond. Both are extremely liquid, which is crucial during these turbulent times and both have low fees of just 0.15%.

You can see SHY has provided a cumulative return of 1.42% over the past 52-week, with all of that coming from yield, which has more than offset the decline in the underlying price.

{kind=link}

The rate at which this recalibration occurred qualified as a 10 sigma move – that would be 10 standard deviations from the 12 month expectations – and is leading many analysts to believe this is the end of the tightening cycle and we will see a further normalization of the yield curve in the next year or so.

One way to play this would be to go long on TLT, while selling, or shorting, SHY. For those looking to limit risk, and possibly add some leverage for higher returns, using options tied to TLT and SHY could make sense.

Both have very liquid options with high daily trading volume and tight bid/ask spreads. To set up a position with a well defined risk one should consider buying or using debit option strategies, which limits the potential loss to the cost or amount spent on the options.

If one is expecting a further reversion from the inversion, you could buy calls on TLT, which will benefit from a rise in price/drop in yield versus buying put options on SHY.

While both TLT and SHY should trend in the same general direction such a position will benefit if TLT rises more relative to SHY. This type of paired action also provides a hedge against a sharp adverse move in one direction.

You can use Magnifi Personal to find and analyze these funds, as well as other bond based ETFs such the more obscure Invesco Senior Loan (BKLN), which tracks an index of leverage loans tied to corporate bonds.

Once you find other options you are interested in, you can even have your personal AI investing assistant compare investments, highlighting the important data points of each selection.

Let Magnifi help you unlock a level of investing you had only dreamt about before. Now the power of an AI assistant is in the palm of your hand.