Better Dividend Stock: Altria (MO) vs. British American Tobacco (BTI)?

Share

{kind=link}

Defensive stocks are those that provide consistent dividends and stable earnings regardless of the state of the overall stock market. There is a constant demand for their products, so defensive stocks tend to be more stable during the various phases of the business cycle. These stocks have yet again proved their resiliency throughout the market’s volatility in the past 18 months.

Today, I will analyze two of the main players in the tobacco industry, Altria Group (MO) and British American Tobacco PLC (BTI) to identify which defensive stock is the better investment.

Altria Group Inc. (MO)

Altria Group, Inc. is a holding company, manufacturing and selling cigarettes, oral tobacco products, and wine in the United States. It offers cigarettes primarily under the Marlboro brand; cigars under the Black & Mild brand, moist smokeless tobacco products under the Copenhagen, Skoal, Red Seal, and Husky brands, as well as oral nicotine pouches. The company also produces and sells a variety of blended table wines and sparkling wines in the United States.

In addition, it provides finance leasing services primarily in transportation, power generation, real estate, and manufacturing equipment industries. The holding company also owns a 10% share in Anheuser-Busch InBev (ABI), one of the world’s largest brewers with a portfolio of over 500 beer brands.

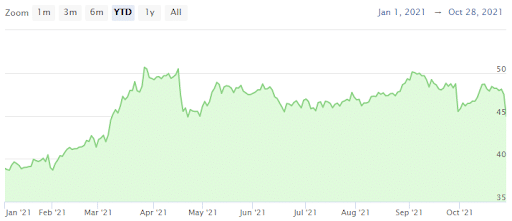

Since the beginning of the year, MO’s shares advanced 7.5%.

Recently, MO released its 3Q2021 earnings report, raised by 5% the lower-end full-year 2021 guidance, and expects to deliver adjusted diluted EPS in a range of $4.58 to $4.62, from a $4.36 base in 2020. The company also announced the expansion of its existing $2b share buyback program to $3.5b, providing additional support for MO’s shares.

With these announcements, investors’ appetite for MO’s stock should continue to rise this year despite flat top line expectations. Indeed, in 2021, MO’s revenues are expected to lift slightly, up only 1.5% to $21.15b, but MO’s top-line growth pattern should maintain a flattish trajectory in the next two years.

On the other hand, MO’s net income has surged this year, posting a massive expansion of 75% year-on-year to $7.81b. Nevertheless, this exceptional boost is unlikely to last, as analysts’ expectations indicate that MO’s bottom line is estimated to grow slightly lower in the next two years, up respectively 9.9% to $8.59b in 2022 and 5.2% to $9.03b in 2023, corresponding to an enormous net margin of 42.3%.

The holding company nevertheless has a comfortable financial structure. With net debt of $25.18b in 2021, MO’s is expected to reduce it marginally next year, down 1.2% to $24.87b, representing a low leverage ratio of only 1.98x.

With these healthy financials, MO trades at relatively low valuation metrics compared to other industries. Indeed, at its current price, MO’s 2022e EV/EBITDA stands at only 9.03x and its 2022e P/E ratio is at 10.2x. Moreover, MO provides a comfortable yearly dividend yield of 7.39%.

British American Tobacco PLC (BTI)

BTI is a holding company that provides tobacco and nicotine products. Its Potentially Reduced-Risk Products (PRRP) include vapor, tobacco heating products (THP), modern oral products including tobacco-free nicotine pouches, as well as traditional oral products such as snus and moist snuff.

Its THP includes Glo, Neo sticks and its vapor products include Vype, Vuse, Ten Motives, and ViP. The company’s international and local cigarette brands include Vogue, Viceroy, Kool, Peter Stuyvesant, Craven A, Benson & Hedges, John Player Gold Leaf, State Express 555, and Shuang Xi.

Earlier this month, BTI received the first of its kind U.S. Food and Drug Administration (FDA) marketing authorization for vapor products, authorizing the sale of its U.S. subsidiary Reynolds’ Vuse Solo product in Original flavor, representing a significant regulatory milestone for the company. While this adds a layer of credibility to the industry’s intended to transition from smoking to vaping, the vaping industry remains a fraction of the size of the smoking market.

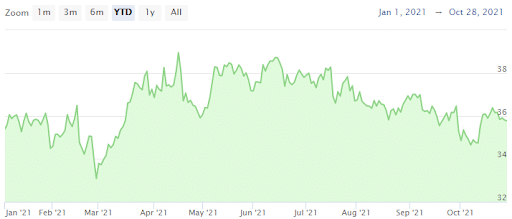

Despite this, BTI had a poor stock performance year in 2021, as investors fled the tobacco giant. Share of BTI declined 6.8% year-to-date, underperforming MO.

However, analysts’ top-line expectations indicate a slightly better expansion than its peer MO. Indeed and while BTI’s net sales should decrease marginally in 2021, down 0.6% to £25.6b, going forward, BTI’s revenues are estimated to lift by 3.8% in 2022 to £26.59b and by 4.3% to £27.73b in 2023.

The company’s bottom line expectations are less attractive, as net income is expected to advance below the 10% range in the next 2 years, up 7.1% to £7.5b in 2022 and up 9.4% to $8.2b in 2023, representing a net margin of 29.6%.

Moreover, BTI is expected to post a net debt of $38.42b in 2021, but it should reduce it by 5% per year until 2023 to $34.29b. However, BTI’s balance sheet is more fragile than MO’s, as its leverage ratio stands higher than MO, at 2.52x.

In terms of valuation, the tobacco giant trades at a discount compared to its peers, with a 2022e EV/EBITDA of 7.56x and a 2022e P/E ratio of 7.88x. Besides, at its current price, BTI provides a higher dividend yield of 8.41% per year.

Take away

MO and BTI share performance diverged this year, even while both companies have high net margins and generate enormous amounts of cash.

MO’s overall financials are more attractive than BTI, but the former is trading at a premium that makes it less attractive in the long term.

It is my belief that BTI looks like the better dividend stock when comparing the two, providing lower valuation metrics, a greater dividend yield, and a better rerating potential after this year’s dull stock performance.