Is Vale a Buy Under $15?

Share

{kind=link}

The price of iron ore has lost more than 40% in the past three months, following weakened demand from China.

Vale S.A. (VALE), a global producer of iron ore, iron ore pellets, and nickel was unable to avoid the negative impacts brought about by this price correction, even if it managed to limit it.

VALE, which extracts other ferrous metals such as manganese and ferro alloys, also mines precious metals such as copper, gold, silver, cobalt, precious metals, which helped buoy the stock and limit the recent decline of its share price.

Since the beginning of the year, VALE lost 12.7%, underperforming its benchmark the SPDR S&P Metals & Mining ETF (XME), which gained 27.65% year-to-date.

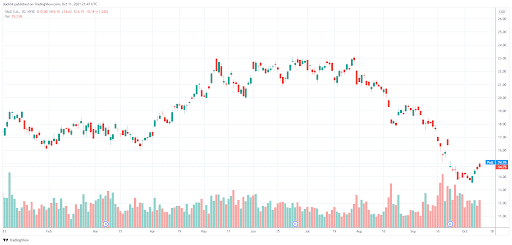

Source: Trading View

The company’s stock has suffered from its less than impressive operating activity in the past years, weighing heavily on its valuation.

Today, I will analyze the company and identify if investors should buy this iron ore giant below $15 per share.

The market is discounting VALE, despite improving financials

In terms of financials, VALE is expected to post a strong top-line performance in 2021. Net sales should rise by 47.12% to $58.8b, according to the consensus of analysts, before dipping 16.9% in 2022 to $48.8b.

On the other hand, VALE’s bottom line should skyrocket in 2021, up more than 5x to $25.3b. However, going forward, VALE’s revenues should take a hit in 2022, declining by a whopping 32.3% to $17.1b, which still represents a comfortable net margin of 35.1%.

While the company’s profitability should decline in 2022, its balance sheet remains healthy. The company transitioned from a net debt position of $3.8b in 2020 to a net cash position of $5.2b in 2021. In addition, the iron ore specialist more than doubled its free cash flow generation in the past year, reaching a value of $22.6b, compared to $9.8b in 2020.

In spite of these strong financials, the market is currently undervaluing VALE, mainly due to the numerous setbacks it faced in base metals operation in the past months.

With a 2022e P/E ratio of 3.61x and a 2022e EV/EBITDA of 2.26x, the iron ore company is cheap and investors should take advantage of this opportunity to benefit from the rerating of the company.

The company’s history of setbacks in base metal operations has negatively affected its valuation, but VALE is addressing these safety issues

VALE has a poor operating track record, with multiple hiccups occurring in the past, indicating the high risk associated with owning shares of this mining company. In 2019, the collapse of the Brumadinho Dam killed 270 and caused catastrophic environmental damage, fines, and complicated legal proceedings, which continues to weigh on the company’s valuation and is fresh in investors’ minds.

Recently, additional setbacks have continued to weigh on the company’s equity value. Miners became trapped in a Canadian mine, a fire was declared at Brazil’s Salobo copper mine and Onca Puma nickel mine was temporarily halted, following the suspension of its operating license by the Environmental and Sustainability office of the Para state.

Nevertheless, VALE has gone through a broad safety review of the operational process, resulting in a comprehensive overhaul of maintenance standards, procedures, training, and oversight. It anticipates improvements from maintenance activities to materialize throughout the business this year.

VALE sees an opportunity to grow in the electric-vehicle supply chain as the world tries to reduce the consumption of fossil fuels. Indeed, it’s copper and nickel mines should unlock additional value for the company as the world transitions towards clean energy.

Conclusion

VALE under $15 per share presents an opportunity for long-term investors, provided the company is able to deliver additional value by supplying metals intended for the electric vehicle market.

Using their expertise to mine metals that are essential for an industry such as electric vehicles means the company can continue to bring in revenue when market conditions surrounding their more traditional products shift. Successful product diversification, as well as tightening up their existing business model, I believe, makes VALE a buy at current prices.